|

|

|

|

Welcome to Week 64 of Be the Change!

The Federal Reserve has raised rates another 25 basis points just Solar loan volume at Capital Good Fund has begun to soar. While understandable--inflation is an issue that needs to be tamed--the Fed's policy has created a bit of a conundrum for us: we need to charge higher rates to be able to raise capital, but higher rates may put the product out of reach for the families we seek to serve. This week I explore the challenge in detail, and, as usual, share a poem.

|

|

|

|

|

|

|

|

|

When Capital Good Fund launched the DoubleGreen Solar loan, in Fall 2021, the Federal Funds Rate (FFR) was near-zero, and we priced the product accordingly: by charging borrowers an APR of 3.099% - 4.99%, we could provide a return of 3% to our capital providers (i.e., those that lend us money)--a solid yield at the time. Since then, however, the FFR has soared to 4.58%; investors are expecting to earn over 7%.

|

In response, solar lenders like Goodleap, Mosaic, and Dividend, have dramatically raised prices through a combination of increased hidden dealer fees (a barely legal tactic I wrote about in Residential Clean Lending's Dirty Secret) and higher interest rates. To put a number on it, a year ago one could get a solar loan with a (hidden) dealer fee of 20% and an interest rate as low as .99%; in some cases, today that fee is 40% and the rate is 2.99% or more. The practical impact is that for a typical $35,000 solar system, the monthly loan payment has gone from $158 to $232, which can easily be the difference between realizing year-one utility savings, and not.

|

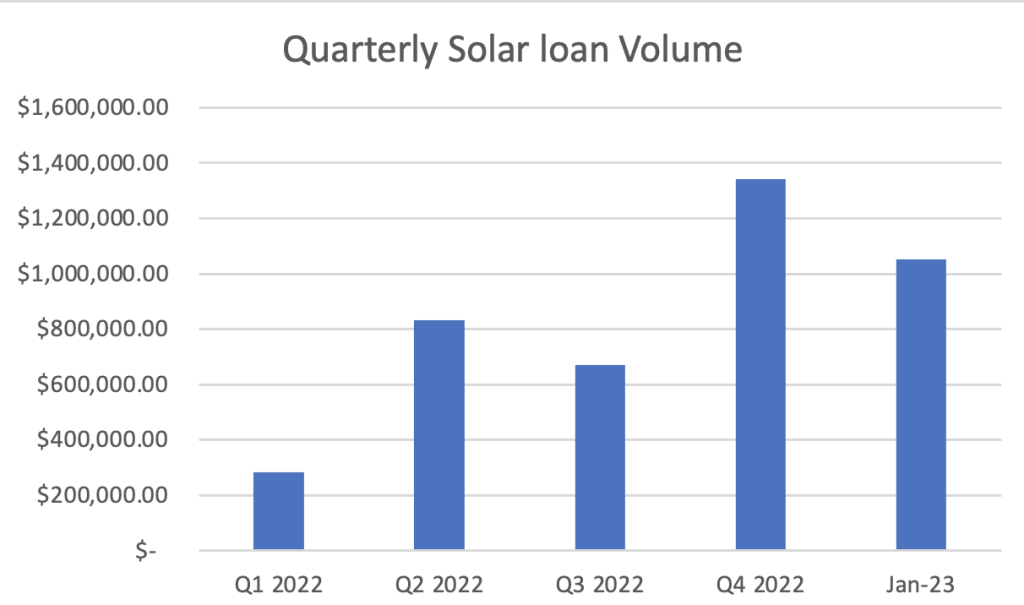

I've written before about why high interest rates are a climate problem; they're now becoming both that and a Capital Good Fund problem! While we have raised our rates once already, by 100 basis points (one percentage-point), we have done so far less than other lenders. Perhaps because of that, in the fourth quarter of last year, Solar loan volume began to soar, and that trend has only accelerated in the past month:

|

|

|

As you can see, we've almost done as much in January of this year as in all of Q4 last year, and Q4 was a huge increase over all prior quarters. So what's the problem? First, the yield we can offer on these loans is below-market, which is making it hard to sell them; if we can't sell them, we can't raise capital to fund additional loans. And while I'm confident we'll be able to find a buyer for the roughly $4 million we've originated, the second conundrum gets at the crux of the challenge of social enterprise--balancing revenue generation with social impact. As it is, just 50% of our solar-loan clients have been low-income (another 20% are moderate-income, defined as 81% - 120% of Area Median Income). That's much better than other lenders, but lower than our target of 60% going to low-income homeowners.

|

So if we raise rates, we can more easily sell the loans, but we risk making it even harder for lower-income families to go solar. For the families we seek to serve, environmental benefits aside, solar has to save them money to be worth it. The higher the rate we charge, the less likely that becomes (although rising energy prices and steadying solar costs can blunt this dynamic). For higher-income families, higher rates are less of a concern. For one thing, many plan to pay down the loan (or pay it off) when they receive the 30% solar tax credit next year. For another, day-one savings aren't as much of a concern for them as savings over the 25-year life of the system.

|

How, then, do we make the product accessible to families and attractive to investors? One option is to offer a two-tiered rate, like 7.99% for regular clients and 6.99% for income-eligible applicants: blending the two still allows us to pay more to investors while, hopefully, keeping the program viable for our target customer. Another option is to raise rates across-the-board and then evaluate the impact. I like several things about this option: it gives us time to collect real-world data on how consumers react to the change; it (hopefully) slows down volume overall, giving us more breathing room to raise capital; and it's much simpler to implement than a tiered system--less training for installers, less work for staff, and less to explain to customers.

|

Finally, we expect money from the Bipartisan Infrastructure Bill and, especially, the Inflation Reduction Act to enable us to lower costs in a variety of ways. For example, the $27 billion Greenhouse Gas Reduction Fund may allow us to raise loan loss reserves or loan guarantees, which should bring down our borrowing cost. The EPA has made available $30 million is environmental justice grants, which we could use for customer education and outreach, among other activities that can bring more underserved families into the pipeline. And we are in talks with a number of other stakeholders, from cities and towns to green banks and more, to ensure that we can continue to reach those who stand to benefit the most from clean energy.

|

|

It's an incredibly difficult balancing act, but it's why organizations like Capital Good Fund exist. If it were easy, it would have been done already. What approaches would you take, if you were in my shoes, to raise capital without pricing low-income families out of the solar market? And if you are reading this and are interested in earning 4.75% - 5.25% by investing in our Solar loan, please reach out to me: andy@capitalgoodfund.org or 401-339-5437!

|

|

|

|

|

|

|

|

|

I Fear Nothing More Than Wasting Time

I'll be brief, for we are both busy

and the calendar Gods have laid waste to

that idyllic peace which, if we're honest,

is as foreign to our forebears as to us.

|

Yet there are moments in our backbreaking

lives on this backbreaking Earth that, were

we to behold them to their utmost, would

call into question this whole endeavor:

|

Not just the raking of leaves, not just work

or self-improvement, but poetry, even love.

Rushing through the dark, a wolf snarls my

name and I don't flinch—I just stand in awe.

|

|

|

|

|

|

|

|

|

|

|

|